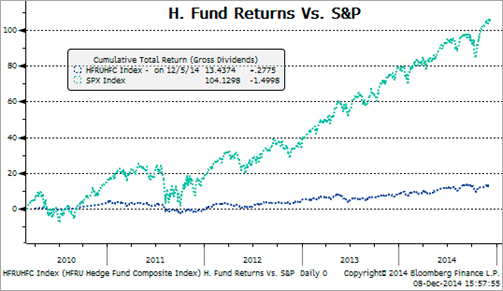

The aggressive pace of government regulation in the United States and the E.U. of the Alternative Investments industry since the onset of the financial crisis of 2008 has had a significant impact on the industry and will continue to do so.

This is likely to affect investors in Alternatives, including hedge funds, private equity funds and other Alternative vehicles, through lower rates of return as the expense ratios of managed products increase in response to new regulations. It is also likely that smaller funds (i.e. with assets under management below $100 million) will seriously consider their viability or possibly be consolidated into larger funds.

The pace of regulation will also make it more difficult for new entrants into the funds management arena. The myriad regulations have been characterized by regulators as being in the best interest of investors and it cannot be argued that investor safeguards are always welcome, particularly for investors who give priority to capital preservation over seeking outsized rates of return.

However, the Alternatives industry was singled out by politicians and regulators in the aftermath of 2008 as the principal culprit in the collapse of global capital markets. The Madoff scandal was cited often as an example of what could go wrong without adequate supervision and regulation. To be sure, there have been notable cases of excessive leveraging in risky markets and, if there are enough of these incidents, systemic risk is inevitable. However, little mention has been made of the overwhelming majority of asset managers in the Alternatives space that have not been in trouble.

Whether or not the Alternatives industry has been a convenient political scapegoat since 2008, the reality is that many new regulations have been enacted and the general expectation among industry players and service providers (structuring attorneys, auditors, administrators, custodians) is that more is on the way, even before the actual impact of current regulations has been fully digested by the industry.

Whether or not the Alternatives industry has been a convenient political scapegoat since 2008, the reality is that many new regulations have been enacted and the general expectation among industry players and service providers (structuring attorneys, auditors, administrators, custodians) is that more is on the way, even before the actual impact of current regulations has been fully digested by the industry.

In the U.S. asset managers with more than $150 million in assets under management must become Registered Investment Advisors, and in many cases must add new permanent staff. New regulations include, in the U.S., Form PF and FATCA.

In the E.U., there is the Alternative Investment Fund Manager Directive (AIFMD), with its Annex 4 reporting requirement. Many E.U. based managers will also need to appoint an independent Depositary (banks with large balance sheets), which will be fully liable to investors if their assets go missing. And there are others. As may be imagined, whether asset managers or the funds they manage bear the cost of engaging outside service providers to comply with the onslaught of new reporting to regulators, it is ultimately investors who will bear the cost in the form of reduced investment returns.

Going forward, investment decisions – which asset managers and/or funds to select – will require more research than in the past to understand the likely impact of regulatory matters on returns. In this environment, one viable option may be for investors to consider placing their liquid assets seeking discretionary management in a custody account with a first-tier custodian and then grant a trading authorization to the asset managers they evaluate and appoint.

Carlos E. Castellanos, Dublin

carlos.castellanos@gencapco.com

+353 085 781 8061