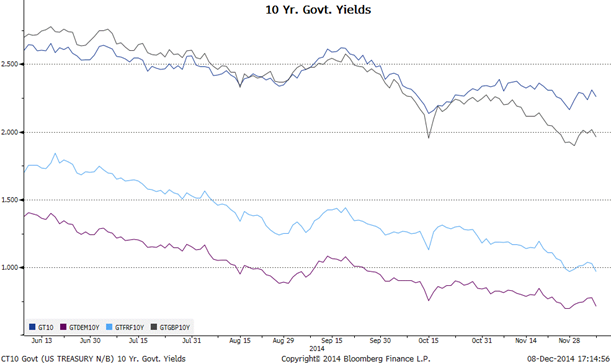

Underpinning the general outlook for interest rates are the growth rates in the United States and Britain, which are significantly higher than those in the E.U. as a whole.

While the United State and Britain posted increases in GDP growth in Q3 of 2014 of 2.4% and 3.0%, respectively, the Euro zone overall posted a .8% growth. Germany and France posted increases, respectively of 1.2% and .4%, while Spain, beginning to show some signs of improvement, registered growth of 1.6%. Italy remains in the doldrums, registering a decline of .4%.

In these circumstances, there is limited pressure on the European Central Bank to make any dramatic changes in monetary policy and interest rates.

While it is not clear that easing rates in the Euro zone further would be a stimulant to economic growth, raising them would likely choke off growth in an economic area that is sluggish at best. 10-year bond yields in the United States and Britain are currently around 2.25% and 2.20%, respectively, while in Germany and France they are around .75% and 1%, respectively.

In the United States, while there seems to be little appetite at the Federal Reserve for an increase in rates, there is certainly considerably less chatter in the news about Quantitative Easing than was the case in the past several years and until a few months ago.

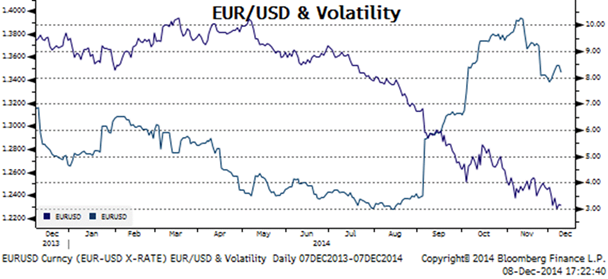

In these circumstances, with comparative weakness in the Euro zone and little likelihood of an increase in interest rates, it is perhaps no surprise that the Euro has been under steady pressure against the U.S. dollar throughout 2014.

From close to 1.40 in the first quarter of this year, the Euro has slipped more or less steadily to around 1.25 currently. From a longer perspective, the absolute decline of the Euro against the U.S. dollar has been more dramatic, from close to 1.50 in 2011 to 1.25 currently.

Beyond economic woes in many sector of the Euro zone, Russian aggression in the Ukraine, and the fear in Germany and other Euro countries that it could spread to other regions, undoubtedly has contributed to weakness in the Euro rate and the near term outlook is for more of the same.

Carlos E. Castellanos, Dublin (carlos.castellanos@gencapco.com | +353 085 781 8061)